New article from Tatton Investment Management: Market sentiment rebound

16 September 2019, 12:00am

Certainly, the uptick in equities cannot have been due to company earnings. We saw an ever-so-slight pickup in earnings expectations for this year and the next – mainly for US businesses – but you would have to squint hard to see this as a trend. Rather, investors seem to have decided that equity markets have been right and bond markets wrong over the summer and now is the time to put their money to work – before the actual economic data improves and they miss the boat.

The current mismatch between market sentiment and company performance can be seen in equity valuations, which, despite mostly unchanged near-term earnings expectations, have moved back up towards recent highs. The economy has not changed, but confidence in it has. Or putting it in market terms, the majority of investors seem to have concluded that the gloominess emanating from rock bottom bond market yields over the summer was perhaps exaggerating the depth and tenure of the ongoing economic slowdown.

The question is, of course: is that confidence justified?

When looking just at indicators like business survey data, one would probably say no. But as we have pointed out recently, markets are increasingly having to take cues from politicians as well. The US-China trade war – one of the biggest concerns for investors for nearly three years – looks as though it may be cooling down. Equities reacted positively to the improved tone of discussions between the world’s two largest economies. In particular, Trump’s removal of former US National Security Advisor John Bolton – an unapologetic war hawk and China hardliner – was taken well. And sure enough, shortly after his departure from the White House, the Trump administration announced delays to scheduled tariffs on China.

Politically, the timing is looking better for a trade deal. Trump is desperate for good news to bring to the American people (his approval ratings are as low as they have ever been). And the continued weakness of the Chinese economy means Beijing will be eager to join the negotiating table.

Elsewhere, the political situation looks rosier too. The prospect of an imminent no-deal Brexit looks less likely, after Parliament closed down the ‘easy’ routes to a 31 October divorce. European political risks (Italy) have also subsided and there are continued rumblings of fiscal expansion on the continent – especially from the ultra-hawks - Germany. A call for looser European fiscal policy has come from Mario Draghi himself – who in his final weeks as ECB President has mustered just about every tool the central bankers have to boost growth through monetary stimulus, but noted their increasingly diminishing effectiveness in the absence of accompanying fiscal support.

Increased growth expectations certainly seem to have impacted the bond market, where yield curves (the plot of a governments’ bond yields at different length maturities) have been steepening rather than flattening for the first time in months across the world. Perhaps equity markets are taking signals from the bond market – rather than politics or underlying company or economic data. The rise of bond yields this week probably also had a lot to do with the record-breaking issuance (capital raising) in investment grade bonds, and a much quieter (but still significant) issuance in high yield debt. All of this could be good news for equities, as the proceeds will go some way to funding dividends (and share-buybacks!).

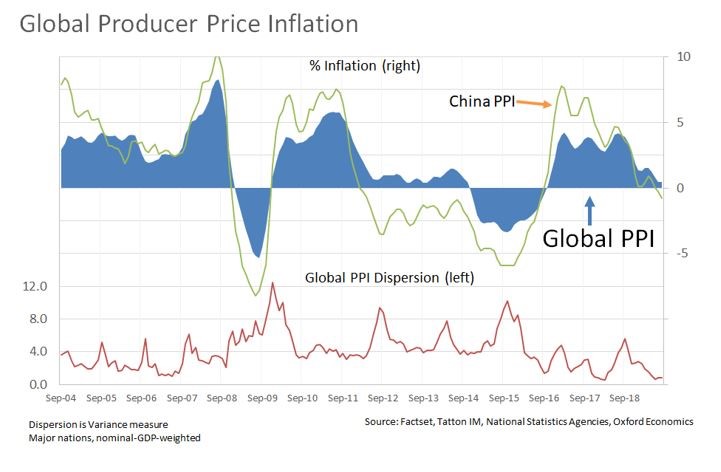

It would be better for the underlying economy, however, if that abundant capital was used to fund productive business investment. Until that happens (or until governments take the responsibility on themselves) it is hard to see a way toward a re-acceleration of global growth. Economic data has stabilised somewhat, but there are signs that businesses are struggling to re-invigorate profit growth. Producer price inflation (PPI) is usually a good proxy for company profitability, and it has been lagging recently.

Nowhere is this more apparent than in China. Chinese PPI – a key signal of company pricing power – came out negative year-on-year for the second month in a row, with a reading of -1%. This is a worrying sign, and it is hard to see how it would improve in the short term. The importance of China here should not be understated. When Chinese companies have an overcapacity, they push that excess stock out to the rest of the world – creating a global oversupply and subsequent drop in prices. This creates a deflationary environment which severely dampens growth prospects. Particularly vulnerable are European producers, which creates a knock-on effect.

The chart below shows our measure of average producer price inflation for the world’s top 10 nations by nominal GDP. China is the most influential component and the second largest. It dominates the average not only because of its size but because it is the major competitor, essentially driving the pricing power of the other. What the dispersion measure shows is that more nations than ever are now being affected by the Chinese lack of pricing power. National PPI measures have declined in unison since the start of the year.

Fortunately, Chinese government officials are acutely aware of this. And given the ongoing difficulty in the domestic economy, they are determined not to let the downturn get worse. Officials in Beijing have already loosened fiscal and monetary policy and taken measures to support consumer demand and small businesses.

What’s more, next month marks the 70th anniversary of the People’s Republic founding and will see a hugely important central party plenum take place. For investors, this is good news. The government usually lends heavy support to the economy around important dates and events, and has already showered traders with ‘gifts’ such as lifting barriers on foreign investment, cutting banks’ reserve requirement ratios and fixing the RMB’s daily trading band at a higher-than-expected level for 17 days. Ever since 2004, the month leading up to big anniversaries has seen the Shanghai Composite Index increase by an average of more than 4%. All of this has made Chinese shares the world’s top performers recently. According to chief strategist at Bocom International Holdings Co. Hao Hong, “Authorities will definitely try to maintain order, and the bottom line is we’re unlikely to see any big declines,â€

Whether that will translate into a sustained pickup in the economy, however, is another matter. We are in a delicate balance, with supportive policies and high political hopes on the one side, and the reality of struggling businesses on the other. But for now at least, the fact that markets think that high hopes will win out is a positive sign.

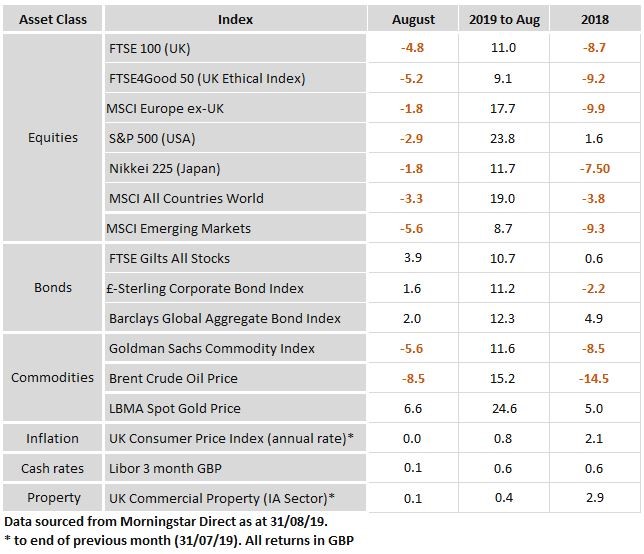

For the time being we are pleased that 2019 investment returns continue to build up well for our investors. (See August asset class table below and positive start for September, bar bonds) . However, as the market sentiment roller-coaster over the summer months has shown, the returns picture will remain volatile until it becomes more evident that improvements in risk asset valuations are founded on actual earnings improvements through economic growth, rather than on hopes and dreams that politics will finally end its sabotaging of the economy, and that the ongoing slowdown is just that, another mid-cycle slowdown and not the beginning of the end of this long-in-the-tooth cycle.

News Archive

19 July 2024, 05:00pm

Latest news from Tatton Investment Management: Shock, rotation, growth?

12 July 2024, 04:00pm

Latest news from Tatton Investment Management: Lower inflation, less profits?

5 July 2024, 05:00pm

Latest news from Tatton Investment Management: New government, same economy

21 June 2024, 04:30pm

Latest news from Tatton Investment Management: Stock market highs don’t feel so high

14 June 2024, 05:00pm

Latest news from Tatton Investment Management: Still mostly sticking to the plan

7 June 2024, 05:00pm

Latest news from Tatton Investment Management: ECB’s Lagard makes rate cut history

31 May 2024, 05:00pm

Latest news from Tatton Investment Management: Markets consolidate

24 May 2024, 04:00pm

Latest news from Tatton Investment Management: Nvidia versus the Fed

17 May 2024, 05:00pm

latest news from Tatton Investment Management: Pluses and minuses

10 May 2024, 05:00pm

latest news from Tatton Investment Management: A blooming May for the UK

3 May 2024, 05:00pm

latest news from Tatton Investment Management: Still sticking to the plan

26 April 2024, 05:00pm

latest news from Tatton Investment Management: Inflation, a common side effect of growth

19 April 2024, 12:00am

latest news from Tatton Investment Management: Market quiet on the Middle Eastern front

12 April 2024, 05:00pm

latest news from Tatton Investment Management: What the return of volatility tells us

5 April 2024, 05:00pm

latest news from Tatton Investment Management: Bumpy start to the quarter

29 March 2024, 05:00pm

latest news from Tatton Investment Management: Everyone is an optimist now

22 March 2024, 05:00pm

latest news from Tatton Investment Management: Stick to the plan

15 March 2024, 05:00pm

latest news from Tatton Investment Management: The flipside of inflation - growth

8 March 2024, 05:00pm

latest news from Tatton Investment Management: At least currency markets noticed the budget

1 March 2024, 12:00am

Latest news from Tatton Investment Management: Winners and losers of stabilising yields

23 February 2024, 05:00pm

Latest news from Tatton Investment Management: M&A activity sets growth against value

16 February 2024, 12:00am

Latest news from Tatton Investment Management: UK not growing really, not growing nominally

9 February 2024, 05:00pm

Latest news from Tatton Investment Management: US stock market entering bubble territory?

2 February 2024, 05:00pm

Latest news from Tatton Investment Management: Central banks challenge Goldilocks assumptions

26 January 2024, 05:00pm

Latest news from Tatton Investment Management: Positive growth sentiment returns

19 January 2024, 05:00pm

Latest news from Tatton Investment Management: Data versus Davos

12 January 2024, 05:00pm

Latest news from Tatton Investment Management: A bumpy upwards path ahead

5 January 2024, 04:40pm

Latest news from Tatton Investment Management: After the party, the hangover?

15 December 2023, 05:00pm

Latest news from Tatton Investment Management: Central bank elves boost 2023 Santa rally

8 December 2023, 05:00pm

Latest news from Tatton Investment Management: A bit of a downer

1 December 2023, 12:00am

Latest news from Tatton Investment Management: Price shock reversal

24 November 2023, 12:00am

Latest News from Tatton Investment Management: Thanksgiving lull

17 November 2023, 05:00pm

Latest News from Tatton Investment Management: Inflation genie back in the bottle?

10 November 2023, 04:00pm

Latest News from Tatton Investment Management: Back pedalling central bankers

3 November 2023, 12:00am

Latest News from Tatton Investment Management: Dovishness proves contagious

27 October 2023, 05:00pm

Latest News from Tatton Investment Management: The resilience narrative comes under pressure

20 October 2023, 05:00pm

Latest News from Tatton Investment Management: Bond yield volatility has markets guessing

13 October 2023, 05:00pm

Latest News from Tatton Investment Management: Capital markets and war

9 October 2023, 09:00am

Latest News from Tatton Investment Management: Recession fears creeping back

2 October 2023, 09:00am

Latest News from Tatton Investment Management: Economic resilience is about to be tested

22 September 2023, 04:00pm

Latest News from Tatton Investment Management: To yield or not to yield

15 September 2023, 05:00pm

Latest News from Tatton Investment Management: Central bank hawks determined to defang inflation

8 September 2023, 05:00pm

Latest News from Tatton Investment Management: Energy in focus - oil prices up and an ill wind for r

1 September 2023, 12:00am

Latest News from Tatton Investment Management: New school term has the US back at the top

25 August 2023, 12:00am

Latest News from Tatton Investment Management: Bonds still calling the shots

18 August 2023, 05:00pm

Latest News from Tatton Investment Management: Bonds are back

11 August 2023, 05:00pm

Latest News from Tatton Investment Management: Summer markets

4 August 2023, 12:00am

Latest News from Tatton Investment Management: Weather matters

28 July 2023, 05:00pm

Latest News from Tatton Investment Management: Rate rises bouncing off 'Teflon' markets

21 July 2023, 05:00pm

Latest News from Tatton Investment Management: Another inflation driver turns over

14 July 2023, 05:00pm

Latest News from Tatton Investment Management: Core inflation slowdown equals an upbeat week for equ

7 July 2023, 05:00pm

Latest News from Tatton Investment Management: Markets sour on news of resilient economy

30 June 2023, 12:00am

Latest News from Tatton Investment Management: A glass half-full half year

23 June 2023, 05:00pm

Latest News from Tatton Investment Management: Markets cathcing up with reality

16 June 2023, 05:00pm

Latest News from Tatton Investment Management: Market conundrum amid volatile growth

9 June 2023, 05:00pm

Latest News from Tatton Investment Management: Immaculate disinflation sentiment cheers investors

2 June 2023, 05:00pm

Latest News from Tatton Investment Management: Markets take good news in their stride

26 May 2023, 05:00pm

Latest News from Tatton Investment Management: Debt ceiling angst or simply lack of good news

19 May 2023, 12:00am

Latest News from Tatton Investment Management:Big tech stocks increase is 'artificial'

12 May 2023, 12:00am

Latest News from Tatton Investment Management: Central bank policy gamble?

5 May 2023, 05:00pm

Latest News from Tatton Investment Management: A small predicament

28 April 2023, 05:00pm

Latest News from Tatton Investment Management: Inflation running out of money

21 April 2023, 05:00pm

Latest News from Tatton Investment Management: Prospects of a warm spring

14 April 2023, 05:00pm

Latest News from Tatton Investment Management: Return of calm bodes well for Spring

6 April 2023, 12:00am

Latest News from Tatton Investment Management: Spring of hope following winter of doom?

31 March 2023, 12:00am

Latest News from Tatton Investment Management: Markets put bank stress behind, but challenges remain

24 March 2023, 12:00am

Latest News from Tatton Investment Management: Swiss parochialism backfires

17 March 2023, 12:00am

Latest News from Tatton Investment Management: Bank stress testing - live

10 March 2023, 12:00am

Latest News from Tatton Investment Management: Market wrestling

3 March 2023, 12:00am

Latest News from Tatton Investment Management: Mood swings

24 February 2023, 12:00am

Latest News from Tatton Investment Management: Balancing acts

17 February 2023, 12:00am

Latest News from Tatton Investment Management: A dose of realism creeps in

3 February 2023, 12:00am

Latest News from Tatton Investment Management: A good month is not a strong year – but it helps

27 January 2023, 12:00am

Latest News from Tatton Investment Management: Goldilocks in the air

20 January 2023, 12:00am

Latest News from Tatton Investment Management: Slowing growth throws markets into a bind

13 January 2023, 12:00am

Latest News from Tatton Investment Management: Football fever saves UK from recession

6 January 2023, 12:00am

Latest News from Tatton Investment Management: January surprises

16 December 2022, 12:00am

Latest News from Tatton Investment Management: Central bank Scrooges cancel Santa rally

9 December 2022, 12:00am

Latest News from Tatton Investment Management: Fed up before Christmas

2 December 2022, 12:00am

Latest News from Tatton Investment Management - Not so bad? Almost good

25 November 2022, 12:00am

Latest News from Tatton Investment Management: Markets give thanks

18 November 2022, 12:00am

Latest News from Tatton Investment Management: Plugging the holes

11 November 2022, 12:00am

Latest News from Tatton Investment Management: Signs of ‘peak inflation’ emboldens markets

4 November 2022, 12:00am

Latest News from Tatton Investment Management: Diverging paths accompanied by seasonally scary messa

28 October 2022, 12:00am

Latest News from Tatton Investment Management: US slows, Europe’s winter outlook improves, UK back t

21 October 2022, 12:00am

Latest News from Tatton Investment Management: The UK and beyond

14 October 2022, 12:00am

Latest News from Tatton Investment Management: Change in the air

7 October 2022, 12:00am

Latest News from Tatton Investment Management: Reading the runes of this week's market bounce

30 September 2022, 12:00am

News from Tatton Investment Management: Loss of trust

23 September 2022, 12:00am

News from Tatton Investment Management: Competing policy measures leave markets worried

16 September 2022, 12:00am

News from Tatton Investment Management: The Fed at work and China snubs Putin

2 September 2022, 12:00am

News from Tatton Investment Management: Waiting for policy action

26 August 2022, 12:00am

News from Tatton Investment Management: Delicate equilibrium

19 August 2022, 12:00am

News from Tatton Investment Management: Will a new PM be good news for investors?

12 August 2022, 12:00am

News from Tatton Investment Management: Fear of missing out

5 August 2022, 12:00am

News from Tatton Investment Management: Markets bet on a perfect landing

29 July 2022, 12:00am

News from Tatton Investment Management: Positive returns amidst negative sentiment

22 July 2022, 12:00am

News from Tatton Investment Management: Economy weakens but central banks persevere

15 July 2022, 12:00am

News from Tatton Investment Management: Too hot, too cold

8 July 2022, 12:00am

News from Tatton Investment Management: Markets not reflecting public fear

4 July 2022, 12:00am

News from Tatton Investment Management: Energy price shock turns into central bank focal point

24 June 2022, 12:00am

News from Tatton Investment Management: Public sentiment vs economic realities

17 June 2022, 12:00am

News from Tatton Investment Management: Linchpin oil price

10 June 2022, 12:00am

News from Tatton Investment Management: Reading between the lines

3 June 2022, 12:00am

News from Tatton Investment Management: Rollercoaster for the Jubilee funfair

27 May 2022, 12:00am

News from Tatton Investment Management: As recession talk subsides, inflation pressures increase

23 May 2022, 12:00am

News from Tatton Investment Management: Talking recession to fight inflation

13 May 2022, 12:00am

News from Tatton Investment Management: Bear market fear as another tech bubble deflates

9 May 2022, 12:00am

News from Tatton Investment Management: Market noise is almost deafening

29 April 2022, 12:00am

News from Tatton Investment Management: Range bound markets - despite the drama

22 April 2022, 12:00am

News from Tatton Investment Management: Finely balanced

14 April 2022, 12:00am

News from Tatton Investment Management: Easter review and outlook

8 April 2022, 12:00am

News from Tatton Investment Management: Q2 begins with QT top of the agenda

1 April 2022, 12:00am

News from Tatton Investment Management: A week of relative calm - and no April fool

25 March 2022, 12:00am

News from Tatton Investment Management: Better news is not always good news

22 March 2022, 12:00am

News from Tatton Investment Management: Changing tides

11 March 2022, 12:00am

News from Tatton Investment Management: Positioning for the energy price shock

4 March 2022, 12:00am

News from Tatton Investment Management: A double edged sword

25 February 2022, 12:00am

News from Tatton Investment Management: Back to the past

18 February 2022, 12:00am

News from Tatton Investment Management: Investors anxious for storms to blow over

11 February 2022, 12:00am

News from Tatton Investment Management: Investment climate change

4 February 2022, 12:00am

News from Tatton Investment Management: The Lagarde pivot hits insecure markets

28 January 2022, 12:00am

News from Tatton Investment Management: Taper Tantrum 2.0 fears rattle markets

21 January 2022, 12:00am

News from Tatton Investment Management: A bumpy road to somewhere

14 January 2022, 12:00am

News from Tatton Investment Management: Markets caught between hoping and dreading

10 January 2022, 12:00am

20 December 2021, 12:00am

News from Tatton Investment Management: Christmas tidings of comfort, if not joy

10 December 2021, 12:00am

News from Tatton Investment Management: Plan B or not Plan B? That is the question

3 December 2021, 12:00am

News from Tatton Investment Management: The pre-Christmas ‘quiz’ that not many want to play

29 November 2021, 12:00am

News from Tatton Investment Management: New COVID variant flattens 'Black Friday' feeling

19 November 2021, 12:00am

News from Tatton Investment Management: Dollar strength and divergence caps a dull week for investor

12 November 2021, 12:00am

News from Tatton Investment Management: Central banks struggle with messaging

5 November 2021, 12:00am

News from Tatton Investment Management: No tantrum over this taper

29 October 2021, 12:00am

News from Tatton Investment Management: Bond markets give central bankers a telling off

22 October 2021, 12:00am

News from Tatton Investment Management: Confused or determined central bankers?

18 October 2021, 12:00am

News from Tatton Investment Management: Have we passed the peak of supply disruption?

8 October 2021, 12:00am

News from Tatton Investment Management: Economy hits an air pocket

1 October 2021, 12:00am

News from Tatton Investment Management: Rising yields are back

24 September 2021, 12:00am

News from Tatton Investment Management: Wall of worry time

17 September 2021, 12:00am

News from Tatton Investment Management: End of the re-opening honeymoon

10 September 2021, 12:00am

News from Tatton Investment Management: Paying for it - major economies ponder their balance sheets

3 September 2021, 12:00am

New article from Tatton Investment Management: Politics and policy sit at the head of the table

27 August 2021, 12:00am

New article from Tatton Investment Management: Fed tapering: the 'how' matters more than 'when'

20 August 2021, 12:00am

New article from Tatton Investment Management: Markets hit a bit of to and fro

16 August 2021, 12:00am

New article from Tatton Investment Management: Climbing the wall of worry - again

11 August 2021, 12:00am

Midas Share Tips: The Daily Mail views onTatton Asset Management

6 August 2021, 12:00am

New article from Tatton Investment Management: Mega techs under the cosh

30 July 2021, 12:00am

New article from Tatton Investment Management: Summer lull as markets go through the motions

23 July 2021, 12:00am

New article from Tatton Investment Management: Markets wake up to living with the virus

16 July 2021, 12:00am

New article from Tatton Investment Management: Earnings vs Delta

12 July 2021, 12:00am

New article from Tatton Investment Management: Don't look down

2 July 2021, 12:00am

New article from Tatton Investment Management:Transition uncertainties

25 June 2021, 12:00am

New article from Tatton Investment Management: Moderating expectations

18 June 2021, 12:00am

New article from Tatton Investment Management: Investors try to make sense of the Fed’s 'dot-plot'

11 June 2021, 12:00am

New article from Tatton Investment Management: Hazy as Carbis Bay

4 June 2021, 12:00am

New article from Tatton Investment Management: Going up sideways

1 June 2021, 12:00am

New article from Tatton Investment Management: Going up sideways

28 May 2021, 12:00am

New article from Tatton Investment Management: Touch of Goldilocks at the end of May

21 May 2021, 12:00am

New article from Tatton Investment Management: Market resilience in face of Bitcoin crash

14 May 2021, 12:00am

New article from Tatton Investment Management: Market vertigo galore

10 May 2021, 12:00am

New article from Tatton Investment Management: Sell in May and go away?

30 April 2021, 12:00am

New article from Tatton Investment Management: Doubling of earnings leaves markets cold

26 April 2021, 12:00am

New article from Tatton Investment Management: Doubling of earnings leaves markets cold

23 April 2021, 12:00am

New article from Tatton Investment Management: 'Risk on' pauses while the real world keeps accelerat

19 April 2021, 12:00am

New article from Tatton Investment Management: New bond news gives green light for equity investors

9 April 2021, 12:00am

New article from Tatton Investment Management: Bond markets signal economic optimism

1 April 2021, 12:00am

New article from Tatton Investment Management: The first quarter of 2021 was no April fool

26 March 2021, 12:00am

New article from Tatton Investment Management: The world is moving on from the pandemic

19 March 2021, 12:00am

New article from Tatton Investment Management: Tug of war - bonds vs. equities

12 March 2021, 12:00am

New article from Tatton Investment Management: Recalibrations

5 March 2021, 12:00am

New article from Tatton Investment Management: Stock markets find they cannot have it both ways

26 February 2021, 12:00am

New article from Tatton Investment Management: Earnings look set to stabilise wobbling markets

19 February 2021, 12:00am

New article from Tatton Investment Management: One year on - who would have thought

12 February 2021, 12:00am

New article from Tatton Investment Management: No UK double dip, but much talk of bubbles

5 February 2021, 12:00am

New article from Tatton Investment Management: Calming of nerves

1 February 2021, 12:00am

New article from Tatton Investment Management: A fraying of nerves

25 January 2021, 12:00am

New article from Tatton Investment Management: A sigh of relief

15 January 2021, 12:00am

New article from Tatton Investment Management: Fiscal turbo replaces lame duck Trump

8 January 2021, 12:00am

New article from Tatton Investment Management: End points and new beginnings

18 December 2020, 12:00am

New article from Tatton Investment Management: Goodbye to all that

14 December 2020, 12:00am

New article from Tatton Investment Management: Outlook 2021 - no deal Brexit?

4 December 2020, 12:00am

New article from Tatton Investment Management: December concerns over baubles and bubbles

27 November 2020, 12:00am

New article from Tatton Investment Management: Fiscal floundering

20 November 2020, 12:00am

New article from Tatton Investment Management: More tunnel before the light

18 November 2020, 12:00am

Interim Results For The Six Month Period Ended 30 September 2020

13 November 2020, 12:00am

New article from Tatton Investment Management: Change is in the air

6 November 2020, 12:00am

New article from Tatton Investment Management: Looking beyond the obvious

4 November 2020, 12:00am

New article from Tatton Investment Management: US Election Update

2 November 2020, 12:00am

New video from Tatton Investment Management: US election, the response to the pandemic and Brexit

30 October 2020, 12:00am

New article from Tatton Investment Management: Unsettled week ahead - or behind

26 October 2020, 12:00am

New article from Tatton Investment Management: Sunlit uplands or COVID gorge?

21 October 2020, 12:00am

New article from Tatton Investment Management: Sunlit uplands or COVID gorge?

19 October 2020, 12:00am

New article from Tatton Investment Management: Watching and waiting

12 October 2020, 12:00am

New article from Tatton Investment Management: Baffling market optimism

2 October 2020, 12:00am

New article from Tatton Investment Management: A question of time horizons

25 September 2020, 12:00am

New article from Tatton Investment Management: A recovery on hold

18 September 2020, 12:00am

New article from Tatton Investment Management: Taking a step back to look forward

14 September 2020, 12:00am

New article from Tatton Investment Management: Frictions and contradictions

7 September 2020, 12:00am

New article from Tatton Investment Management: Market dynamic of a K-shaped recovery

1 September 2020, 12:00am

New article from Tatton Investment Management: Big tech gets bigger while the Fed takes the easy opt

24 August 2020, 12:00am

New article from Tatton Investment Management: Fed leaves bond investors with that sinking feeling

17 August 2020, 12:00am

New article from Tatton Investment Management: COVID II the sequel - as scary as the original?

10 August 2020, 12:00am

New article from Tatton Investment Management: July brings consolidation

2 August 2020, 12:00am

New article from Tatton Investment Management: Sunshine and shadows

27 July 2020, 12:00am

New article from Tatton Investment Management: PPE = Politics, Pressure and Economics

20 July 2020, 12:00am

New article from Tatton Investment Management: Discomfort of disappearing safety nets

13 July 2020, 12:00am

New article from Tatton Investment Management: Fast and freewheeling

3 July 2020, 12:00am

New article from Tatton Investment Management: H1 2020 offers meaningful lessons

29 June 2020, 12:00am

New article from Tatton Investment Management: Support balances increasing strains - for how long?

22 June 2020, 12:00am

New article from Tatton Investment Management: Equity valuations follow bond valuations' lead

15 June 2020, 12:00am

New article from Tatton Investment Management: Stock markets suffer altitude sickness

8 June 2020, 12:00am

New article from Tatton Investment Management: Markets are enjoying an uncomfortably benign pandemic

1 June 2020, 12:00am

New article from Tatton Investment Management: Optimistic markets despite second wave lockdown threa

26 May 2020, 12:00am

New article from Tatton Investment Management: Just as the sun comes out, clouds appear in the East

22 May 2020, 12:00am

New video from Tatton Investment Management

18 May 2020, 12:00am

New article from Tatton Investment Management: Us-China cold war: Threat or blessing?

11 May 2020, 12:00am

New article from Tatton Investment Management: Most welcome, if feeble, signs of pulling together

4 May 2020, 12:00am

New article from Tatton Investment Management: Opening-up will be slower than locking down

27 April 2020, 12:00am

New article from Tatton Investment Management: V or U-shaped recovery scenarios - the jury is out

20 April 2020, 12:00am

New article from Tatton Investment Management: Lifting lockdown remains a delicate balancing act

20 April 2020, 12:00am

New video from Tatton Investment Management: Stock markets between hope and despair

15 April 2020, 12:00am

New video from Tatton Investment Management: Is now the time to invest?

13 April 2020, 12:00am

New article from Tatton Investment Management: Fading threat of financial crisis re-opens old divide

6 April 2020, 12:00am

New article from Tatton Investment Management: Unprecedented quarter or calm before the storm?

30 March 2020, 12:00am

New article from Tatton Investment Management: Extraordinary: bear and bull market all in one

24 March 2020, 12:00am

New video from Tatton Investment Management: Why have stock markets appeared to rally on the lock-do

23 March 2020, 12:00am

New article from Tatton Investment Management: Government ordered recession

19 March 2020, 12:00am

New video from Tatton Investment Management: Confusion reigns in Capital Markets

18 March 2020, 12:00am

New article from Tatton Investment Management: Why aren't you doing something?

17 March 2020, 12:00am

New video from Tatton Investment Management: From euphoric recovery to depressed tumble

16 March 2020, 12:00am

New article from Tatton Investment Management: Notes on a crash: the short, the medium and long term

13 March 2020, 12:00am

New video from Tatton Investment Management: Panic equity selling or panic raising of precautionar

12 March 2020, 12:00am

New article from Tatton Investment Management: Forced sellers and other distractions

9 March 2020, 12:00am

New article from Tatton Investment Management: Dark times or glimpse of light at the end of the tunn

6 March 2020, 12:00am

New article from Tatton Investment Management: News of a reverse oil price shock rattles markets bey

2 March 2020, 12:00am

New article from Tatton Investment Management: Coronavirus - hitting too close to home

28 February 2020, 12:00am

New article from Tatton Investment Management: This week's market correction requires perspective

26 February 2020, 12:00am

New article from Tatton Investment Management: COVID-19 and the reaction of markets to pandemic fear

24 February 2020, 12:00am

New article from Tatton Investment Management: US markets hit new all-time highs and a 'bump'

17 February 2020, 12:00am

New article from Tatton Investment Management: V-shaped recovery for Valentine

10 February 2020, 12:00am

New article from Tatton Investment Management: Markets show no fear - should they?

3 February 2020, 12:00am

New article from Tatton Investment Management: Looking through the noise of the week

27 January 2020, 12:00am

New article from Tatton Investment Management: Short break to Goldilocks?

20 January 2020, 12:00am

New article from Tatton Investment Management: Parallels and differences to January 2018

14 January 2020, 12:00am

13 January 2020, 12:00am

New article from Tatton Investment Management: So far so good

8 January 2020, 12:00am

Tatton: Woodford & M&G suspensions have driven IFAs to us

6 January 2020, 12:00am

New article from Tatton Investment Management: 2020 starts with a Trump card

23 December 2019, 12:00am

New article from Tatton Investment Management: Goodbye 2019 - welcome 2020 and a new decade!

16 December 2019, 12:00am

New article from Tatton Investment Management: Brightening horizons - 2020 Outlook

8 December 2019, 12:00am

New article from Tatton Investment Management: Can Trump derail the 2020 economic upturn?

2 December 2019, 12:00am

New article from Tatton Investment Management: Markets are driving the markets

25 November 2019, 12:00am

New article from Tatton Investment Management: Markets pause for reality check

18 November 2019, 12:00am

New article from Tatton Investment Management: Swilling cash eases the market mood music

11 November 2019, 12:00am

New article from Tatton Investment Management: Recession concerns retreat

11 November 2019, 12:00am

Interim Results for the six months ended 30 September 2019

4 November 2019, 12:00am

New article from Tatton Investment Management: Crucial October period safely behind

28 October 2019, 12:00am

New article from Tatton Investment Management: Slowly turning

21 October 2019, 12:00am

New article from Tatton Investment Management: Brexit breakthrough versus Brexit fatigue

17 October 2019, 12:00am

17 October 2019, 12:00am

Acquisition of Sinfonia Asset Management Limited (SAM)

14 October 2019, 12:00am

New article from Tatton Investment Management: Market sentiment rebound

7 October 2019, 12:00am

New article from Tatton Investment Management: Stall speed economy fears spreading

30 September 2019, 12:00am

New article from Tatton Investment Management: Ominous US-Dollar strength

23 September 2019, 12:00am

New article from Tatton Investment Management: Diverging economic trends - catalyst for trade war re

16 September 2019, 12:00am

New article from Tatton Investment Management: Market sentiment rebound

9 September 2019, 12:00am

New article from Tatton Investment Management: Choppy water but no storm, yet...

2 September 2019, 12:00am

New article from Tatton Investment Management: Fattening 'tails'

27 August 2019, 12:00am

New article from Tatton Investment Management: Populism politics reversing austerity?

19 August 2019, 12:00am

New article from Tatton Investment Management: Market spat between bond and equity markets

11 August 2019, 12:00am

New article from Tatton Investment Management: Bond markets unnerve equity markets - again

5 August 2019, 12:00am

New article from Tatton Investment Management: The Elephant and the Little Old Lady

29 July 2019, 12:00am

New article from Tatton Investment Management: The quick and the not-so-quick

22 July 2019, 12:00am

New article from Tatton Investment Management: ...'Twere well it were done quickly

15 July 2019, 12:00am

New article from Tatton Investment Management: Positioning for a summer of wait and see

8 July 2019, 12:00am

New article from Tatton Investment Management: Liquidity drives stock markets to new highs

1 July 2019, 12:00am

New article from Tatton Investment Management: The middle of the year - a tipping point?

24 June 2019, 12:00am

New article from Tatton Investment Management: Battle of the ‘doves’

17 June 2019, 12:00am

New article from Tatton Investment Management: Mixed messages

10 June 2019, 12:00am

New article from Tatton Investment Management: The return of the central bank put?

3 June 2019, 12:00am

3 June 2019, 12:00am

Appointment by Frenkel Topping

3 June 2019, 12:00am

Preliminary Results For the year ended 31 March 2019

3 June 2019, 12:00am

New article from Tatton Investment Management: Bond rally musings

27 May 2019, 12:00am

New article from Tatton Investment Management: It is getting warmer

20 May 2019, 12:00am

New article from Tatton Investment Management: Market support for Trump or unwarranted equanimity?

13 May 2019, 12:00am

New article from Tatton Investment Management: Geopolitics re-enter market stage

7 May 2019, 12:00am

New article from Tatton Investment Management: Central banks disappoint expectations

29 April 2019, 12:00am

New article from Tatton Investment Management: Waning market stimuli put stock markets on notice

23 April 2019, 12:00am

New article from Tatton Investment Management: Spring time from here?

16 April 2019, 12:00am

Trading Statement for 12 months ending 31 March 2019

15 April 2019, 12:00am

New article from Tatton Investment Management: Brexit in-limbo aside sentiment is improving

8 April 2019, 12:00am

New article from Tatton Investment Management: Happy 10th birthday, choppy bull market

1 April 2019, 12:00am

New article from Tatton Investment Management:29 March 2019 – quarter end

25 March 2019, 12:00am

New article from Tatton Investment Management: Brinkmanship and extensions

18 March 2019, 12:00am

New article from Tatton Investment Management: Bits & Pieces

11 March 2019, 12:00am

New article from Tatton Investment Management: ECB stimulus U-turn leaves markets unimpressed

4 March 2019, 12:00am

New article from Tatton Investment Management: £-Sterling ‘applauds’ prospect of Brexit delay

25 February 2019, 12:00am

New article from Tatton Investment Management: Progress?

18 February 2019, 12:00am

New article from Tatton Investment Management: Investment perspectives for different Brexit outcomes

15 November 2018, 12:00am

Interim Results for the six months ended 30 September 2018

15 October 2018, 12:00am

New article from Tatton Investment Management: Autopsy of a stock market sell-off

1 October 2018, 12:00am

New article from Tatton Investment Management: Poor politics containing bond market risks?

27 September 2018, 12:00am

New article from Tatton Investment Management: Brexit clamour vs. real market new

7 September 2018, 12:00am

New article from Tatton Investment Management: Interesting times ahead

31 August 2018, 12:00am

New article from Tatton Investment Management: “Not the end of the worldâ€

24 August 2018, 12:00am

New article from Tatton Investment Management: Steady markets vs. noisy politics

17 August 2018, 12:00am

New article from Tatton Investment Management: Political strongman tactics come home to roost

10 August 2018, 12:00am

New article from Tatton Investment Management: Summer heat wave makes way for return of political he

3 August 2018, 12:00am

New article from Tatton Investment Management: A gentle deceleration?

27 July 2018, 12:00am

New article from Tatton Investment Management: Hot air for a hot summer?

20 July 2018, 12:00am

New article from Tatton Investment Management:Earnings are growing, why worry?

13 July 2018, 12:00am

New article from Tatton Investment Management: Hard Brexit demonstration potential?

6 July 2018, 12:00am

Notice of Annual General Meeting

6 July 2018, 12:00am

New article from Tatton Investment Management: It is getting hot

29 June 2018, 12:00am

New article from Tatton Investment Management: Digesting or consolidating?

27 June 2018, 12:00am

Preliminary Results for the year ended 31 March 2018

22 June 2018, 12:00am

New article from Tatton Investment Management: Fragile recovery

15 June 2018, 12:00am

New article from Tatton Investment Management: No surprises

8 June 2018, 12:00am

New article from Tatton Investment Management: Delicate equilibrium

1 June 2018, 12:00am

New article from Tatton Investment Management: Ignore politics at your peril

25 May 2018, 12:00am

New article from Tatton Investment Management: GDPR? No - far more interesting news!

18 May 2018, 12:00am

New article from Tatton Investment Management: What's the economic reality of this week's news?

11 May 2018, 12:00am

New article from Tatton Investment Management: Batten-down-the-hatches?

4 May 2018, 12:00am

New article from Tatton Investment Management: Past the peak?

27 April 2018, 12:00am

New article from Tatton Investment Management: Confusing signals?

20 April 2018, 12:00am

New article from Tatton Investment Management: A mixture of messages

6 April 2018, 12:00am

New article from Tatton Investment Management: Could do better

6 April 2018, 12:00am

New article from Tatton Investment Management: Peaking, plateauing or dimming – and how about that

29 March 2018, 12:00am

New article from Tatton Investment Management: End of a stormy quarter

23 March 2018, 12:00am

New article from Tatton Investment Management: Now we know it's risky!

16 March 2018, 12:00am

New article from Tatton Investment Management: Back to Normal?

9 March 2018, 12:00am

New article from Tatton Investment Management: Tariffs to growth

2 March 2018, 12:00am

New article from Tatton Investment Management: Time to take some profits

23 February 2018, 12:00am

New article from Tatton Investment Management: Change of direction or gradual normalisation?

16 February 2018, 12:00am

New article from Tatton Investment Management: Breathing easier for the moment

9 February 2018, 12:00am

New article from Tatton Investment Management: Meteoric stock markets crash bac

6 February 2018, 12:00am

Tatton Investment Management's Stock Market Correction Assessment

2 February 2018, 12:00am

New article from Tatton Investment Management: Good news turns bad news - again!

26 January 2018, 12:00am

New article from Tatton Investment Management: Surprises

19 January 2018, 12:00am

New article from Tatton Investment Management: US$ weakness versus Bitcoin and Carillion

12 January 2018, 12:00am

New article from Tatton Investment Management: Bullish sentiment rings alarm bells

5 January 2018, 12:00am

New article from Tatton Investment Management: Encouraging kick-off

15 December 2017, 12:00am

New article from Tatton Investment Management: 2017 - taking stock

8 December 2017, 12:00am

New article from Tatton Investment Management: Progress versus Bitcoin

5 December 2017, 12:00am

Interim results for the six months ended 30 September 2017

1 December 2017, 12:00am

New article from Tatton Investment Management: Sudden, but not entirely unexpected

24 November 2017, 12:00am

New article from Tatton Investment Management: Invincible markets?

17 November 2017, 12:00am

New article from Tatton Investment Management: Yield-curve flattening: a bad omen?

10 November 2017, 12:00am

New article from Tatton Investment Management: Nervous investors herald more volatile markets

3 November 2017, 12:00am

New article from Tatton Investment Management: UK rate rise: ‘one and done’ or beginning of rate

27 October 2017, 12:00am

New article from Tatton Investment Management: Trick or treat season

13 October 2017, 12:00am

New article from Tatton Investment Management: All-time highs and Q3 results outlook: Reasons to be

6 October 2017, 12:00am

New article from Tatton Investment Management: Bad news – good news

29 September 2017, 12:00am

New article from Tatton Investment Management: Movements

22 September 2017, 12:00am

New article from Tatton Investment Management: QT to reverse QE and 2-year transition period to soft

15 September 2017, 12:00am

New article from Tatton Investment Management: BoE guides for year-end rate hike - Bluff or real?

8 September 2017, 12:00am

New article from Tatton Investment Management: ‘Back to school’ amidst hurricanes, earthquakes

1 September 2017, 12:00am

New article from Tatton Investment Management: Bad news, Good news

25 August 2017, 12:00am

New article from Tatton Investment Management: Summer low or summer lull?

18 August 2017, 12:00am

New article from Tatton Investment Management: More sellers than buyers

11 August 2017, 12:00am

New article from Tatton Investment Management: Stocks take note of North Korea crisis - or do they?

4 August 2017, 12:00am

New article from Tatton Investment Management: Consolidated base but momentum dwindling

28 July 2017, 12:00am

New article from Tatton Investment Management: Summer thoughts about the ‘longer term’

21 July 2017, 12:00am

New article from Tatton Investment Management: Summer lull - delayed

14 July 2017, 12:00am

New article from Tatton Investment Management: Pre summer-holiday investment check

7 July 2017, 12:00am

New article from Tatton Investment Management: Global growth ploughs on while markets take a breathe

23 June 2017, 12:00am

New article from Tatton Investment Management: Quo Vadis Britain?